Category:

Pipeline

Published On:

The Pipeline - Issue 03: Data Centres, Demand, and Delivery

Can the UK’s Planning System Keep Up With AI Ambitions?

A look inside the UK’s data centre pipeline.

The UK is rolling out the red carpet

The UK has declared itself open for AI business. Since publishing its AI Opportunities Action Plan in January 2025, a 50-point roadmap to position the UK as a global leader in AI, the government has designated AI Growth Zones across the country, offering fast-tracked planning and power connections for data centres, and updated the NPPF to require local authorities to actively plan for data centre development, including site allocation and flood risk reclassification. Data centres are now categorised as critical infrastructure.

The investor appetite is there too. In April, the government launched the £500 million Sovereign AI Unit, a state-backed venture designed to keep homegrown AI companies scaling on British soil rather than relocating overseas. And just last week, the Chancellor reminded Cabinet colleagues to "Buy British", highlighting the priority of British companies when awarding government contracts in AI. In 2025, It is estimated that 63% of venture capital investment was directed to deeptech and AI companies.

So, pressure on the demand side is clearly present and only continuing to ramp up. But what about the supply side? Is the planning pipeline responding to this pressure accordingly? That’s what I wanted to pick apart in this edition of Build, Baby, Build, and what sits as a perfect case study for IBex's decision-level planning data - capturing the condition of these major infrastructure projects through to decision.

Where does the infrastructure currently stand?

The UK currently has an estimated 1.6GW of co-location data centre capacity, the vast majority concentrated in London and the South East. The government’s UK Compute Roadmap targets at least 6GW by 2030 - roughly triple what exists today. The government is not directly funding construction; its strategy is to remove barriers to building. The development, then, depends on the planning system.

A widening funnel: What our data shows

The headlines appear to be focused on submission levels only. Using IBex data, we can track the full journey from application to decision across England and Wales. The picture it reveals is nuanced and interesting.

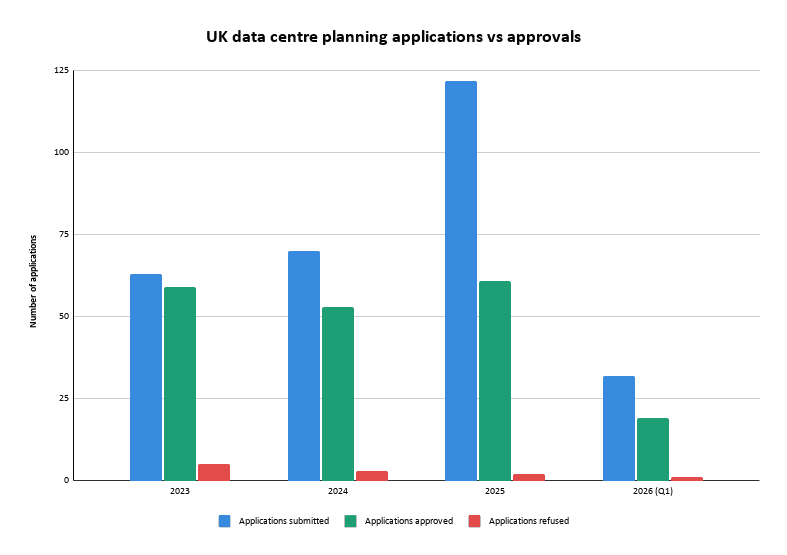

UK data centre planning applications vs approvals, 2023-2026. Source: IBex, Planda Portal

According to our data, In 2023, 63 data centre applications were validated. Of those, 59 were approved - an approval rate of 93.7%. The supply chain was keeping pace with demand.

By 2024, submissions had risen 11% to 70. But approvals actually fell 10% to 53, and the approval rate dropped to 75.7%. More applications were going in; fewer were going out.

In 2025, the gap widened significantly. Applications surged three-quarters to 122 - a clear signal of increased demand. Approvals, however, rose just 15% to 61. The approval rate halved to 50%.

The contrast jumps out from the page: over two years, submission almost doubled whilst approvals stayed pretty much the same. The refusal rate hasn’t spiked, just two applications were refused last year. The growing gap isn’t about schemes being rejected. The correlation appears to align with schemes sitting undecided, or withdrawn. The planning pipeline for UK data centres is filling up faster than it’s draining.

Early data from 2026 suggests that pattern is continuing. In the first quarter alone, 32 applications were validated, putting the year on pace to either match or exceed 2025’s record. The appetite is clearly there. The question is whether the planning system can convert increasing applications into consented capacity at the rate the UK’s AI ambitions require.

Conclusion:

Is the demand there? Without question. AI Growth Zones are expected to fast-track the required infrastructure going through planning, the Chancellor is driving domestic AI procurement,and 63% of UK venture capital investment last year was directed at deeptech and AI. The appetite to build is certainly not the issue.

Is supply keeping up? Not quite. Submissions are surging but approvals appear to be stalling. The planning system isn’t refusing these projects - approval rates remain very high compared to refusals. But it looks like the volume of applications is starting to outpace the ability of local planning authorities to process them. If we want to mitigate the risk of the UK’s 6GW target becoming an aspiration rather than a roadmap, it is important to assist local planning authorities in bridging the gap between the two.

This is where specific operational improvements matter more than some might expect, like faster validation and better-resourced planning teams, meaning officers can spend less time on avoidable errors and more time reaching decisions. These are the kind of day-to-day improvements that can be applied to curb delays whilst wider reform is established.

Subscribe to our Newsletter!